Charities that have investment portfolios and give discretionary powers to an investment manager are required by law to have a written investment policy statement and review it on a regular basis. The Charity Commission provides guidance on what such a policy should include, but the level of detail can vary substantially. In many cases, investment policies can be rather blunt and more than once we have seen policies where return objectives and risk tolerance are not consistent. A policy review can also frequently be a tick box exercise that does not challenge if the investment objectives are still in sync with a charity’s intrinsic demands or realistic in a given macroeconomic backdrop.

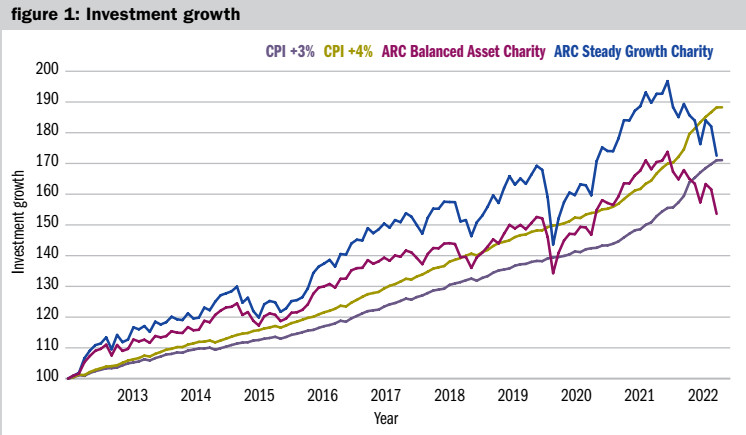

As trustees review their portfolios currently, most are seeing the value of their funds decline and are understandably concerned about inflation and volatility. An average charity portfolio (as shown by the ARC Balanced and Steady Growth Charity Indexes) has fallen short of common inflation-based long-term objectives.

In such an environment it is not surprising that we are seeing an increased demand for a comprehensive review of investment management arrangements and investment policies. However, when the news flow is dominated by the political turmoil and extreme volatility in gilts, which are usually deemed to be safe assets, it is rather difficult to retain a focus on the long-term strategic objectives. Below we explore what has really changed in the world of charity investments and what it means for trustees that are reviewing their investment policies.

Balancing risk and return

While the current market environment is unprecedented on many accounts, from a longer-term strategic perspective, investors were always concerned with matters of inflation eroding the long-term value of funds, volatility of returns and portfolio diversification. In our view, what is changing is that many trustee boards and investment committees had a relatively smooth ride over most of the past decade as their portfolios generated returns well in excess of inflation, enabling them to both preserve the real value of capital and fund annual distributions. The combination of low inflation, low volatility and relatively high returns put little demand on investment strategies, which is no longer the case.

When we work with charities, one of the most important tasks is finding an appropriate balance between risk tolerance and target return. This balance would depend on many factors, including time horizon, cash flow profile, underlying liabilities, operational model as well as organisation culture.

When working with permanent endowments, in most instances charities need to embrace volatility with a view of getting sufficient real returns. The challenges come when a portfolio is not a pure permanent endowment, but has other liabilities attached to it. We find that for trustees to deal with investment risk efficiently, it is important to have sufficient expertise on the committee and provide training to ensure that trustees understand the risks and do not shy away for the wrong reasons, resulting in lower real returns.

Another important consideration for endowment models is ensuring good discipline on annual distributions. With higher inflation and volatility, having a robust model ensuring both stability of annual distributions and preserving the real value of capital is a key. They need to determine what a sustainable distribution rate is going forward. The situation may be different for charities that are starting their endowments afresh compared to those that have enjoyed excess returns in the past decade and can afford to redistribute for some time if required.

Operational charities that need to invest their medium-term reserves face a different set of challenges when dealing with market volatility. With extreme volatility in bonds and still mainly negative real yields, this part of the market remains very challenging. A part of the solution, in our view, is more careful time horizon planning that can help avoid this difficult middle ground as much as possible.

Asset allocation

When talking about asset allocation it is extremely important to distinguish between strategic and tactical decisions. In our view, trustees should be actively involved in the former and not the latter. As an example, over the past few years we have seen a strong trend of taking a strategically global approach to equities and decreased reliance on bonds for portfolio diversification in favour of alternative investments. Tactically, however, it would have been a good investment decision to overweight UK equities in the past year. In fixed income, we are also seeing managers that stayed away from the asset class for years starting to show interest after the recent sell-off.

We believe that it is extremely important for trustees of charities that delegate discretionary portfolio management to professional fund managers to remain focused on the strategy and not be distracted by market moves. In that sense, we believe charities should focus on what they are trying to achieve with their money over the long term and leave it to fund managers to decide when the time is right to invest in bonds.

When it comes to alternative investments, we are seeing significant growth in this group as asset classes mature, become more mainstream and become increasingly accessible to a broader group of investors. These assets can be very diverse in terms of their investment characteristics, some offering premium returns with high volatility, some being linked to inflation or behaving like fixed income. It is therefore important to discuss the objectives and characteristics of the portfolio with your fund manager, rather than labelling alternatives as a group. With the increased focus on environmental, social and governance (ESG) issues and impact investing, private assets that are traditionally part of alternatives also play a significant role.

In the past investing in private assets that focus on making a positive impact on climate change or certain social factors was only possible for very large endowments and foundations. Now a number of managers are starting to offer such opportunities through pooled vehicles with very modest minimum investment levels, making them available for any charity that wants to build an impact portfolio.

ESG and regulatory changes

The biggest development in the regulatory framework was the High Court ruling in April 2022 on the Butler-Sloss case, that provided clarification of the 1992 Bishop of Oxford case that underpins the Charity Commission guidance on ethical and responsible investment.

Technically, the judgment is a clarification of the law and by nature a restatement of the existing relevant legal principles. The Charity Commission had not implemented its draft responsible investment guidance, pending the Court’s decision in this case. However, the proposed changes include a more definitive statement that an investment policy should include whether the trustees have decided to take a responsible investment approach. When addressing ethical and responsible investment, the ruling suggests that trustees should use a balancing exercise on the extent of the conflict and the potential financial effect (including reputational damage).

Combined with an increasing focus on responsible investing and, in particular, the role of the financial sector in addressing climate change, that manifests itself through changes in pension fund regulations and behaviour of private investors, we see that charities that fail to address their stance on these issues can face significant reputational risks.

Implementation

In terms of implementation, the biggest global trend over the past decade is probably the growth of passive investing, which we are now seeing also being increasingly used by charities as well. With index providers, such as MSCI and FTSE being very much involved in the debate around ESG and climate change, it is possible to easily comply with most responsible investment policies through investing in various kinds of screened indexes.

In the UK charity space, we have also seen strong growth in pooled funds over segregated portfolios, which not only offer cost efficient solutions, but also provide access to a range of investments that would be otherwise difficult to implement for an average size charity. We have seen many investment policies that require a segregated approach as a default, where it is not necessarily the best solution for every charity.

Tatyana Mursalimov is director at PMCL Consulting

Charity Finance wishes to thank PMCL Consulting for its support with this article