Since our last update we have seen an opportunistic deal between the Conservative Party and DUP that has somewhat diminished the level of political chaos provoked by the snap election. That said, uncertainties over the shape of a post-Brexit UK remain considerable. Unsurprisingly, this makes for a fragile environment that the Bank of England has to navigate, leaving the near-term path for interest rates uncertain.

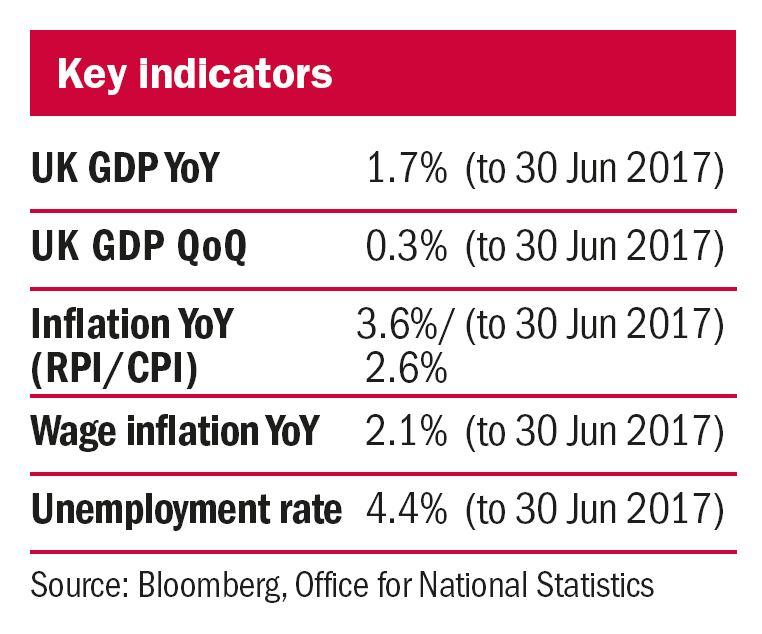

The UK economy has evidently performed better than expected since August 2016, with employment intentions and labour demands remaining strong. Meanwhile, although the global economy may not be growing at the rate desired by politicians and electorates, it continues, in general, to heal. The US, despite a seemingly customary first quarter softness, continues to chug along; eurozone indicators are at a six-year high; and while the Chinese growth story might have long-term structural issues, it continues to defy talk of an abrupt cyclical slowdown.

Policy tightening

This has given many central bankers a motive to start removing some of the loose monetary policy that has dominated markets for the last seven years. Some, such as the Federal Reserve and the Bank of Canada, are further along in this process, having already started to increase interest rates. Others, like the Bank of England, have indicated their desire to raise rates, although a weaker than expected UK inflation figure published in July took an imminent rate hike off the table. Crucially, what they all have in common is the direction in which they are heading.

While global growth data seems robust enough to withstand rising rates, it is unclear whether the equity market will tolerate the move. As a result of quantitative easing (QE), an estimated $12tn has been added to the balance sheets of central banks across the world. This has been hugely positive for equity markets and equity holders alike, as the tide of liquidity unleashed by QE has resulted in almost all stocks moving higher in unison. Signals that authorities are moving towards tighter monetary policy indicates a significant shift in market dynamics, and one that, perhaps, few investors are truly prepared for.

Christopher Querée is investment director and head of charities at Ruffer – www.ruffer.co.uk